Automatic backtesting

no coding required

Define your trading rules in plain English. Get institutional-grade backtest results.

No Python. No spreadsheets. Just your strategy and the data.

Early access + founding user pricing

Powerful backtesting, zero code

Get the insights quants have — without learning to program.

Define your rules

Define your trading rules in plain language — entries, exits, risk, sessions.

Backtest across history

Run your strategy across historical market data instantly.

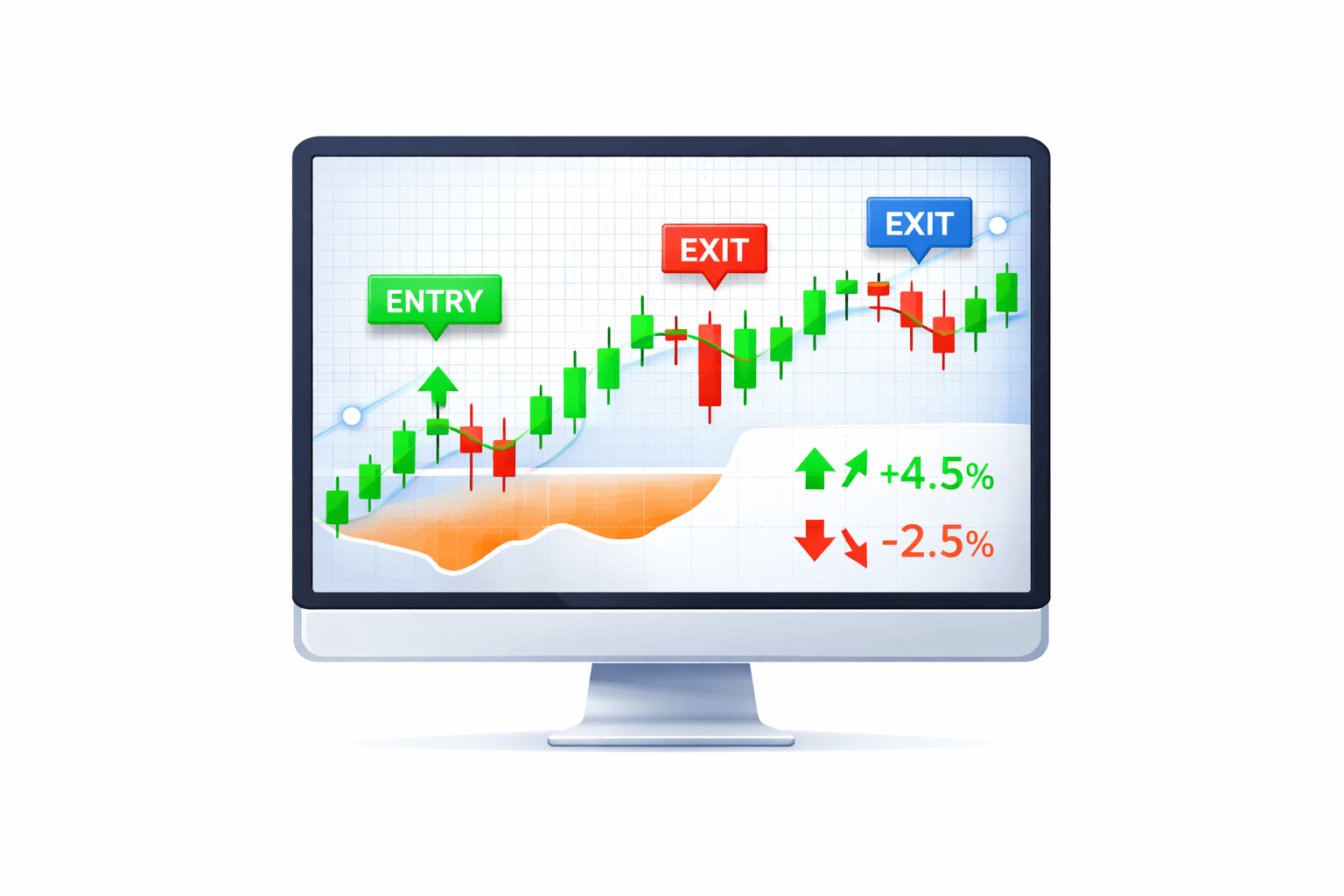

Visualise performance

See entries, exits, drawdown, and expectancy at a glance.

Iterate quickly

Refine your edge without spreadsheets or manual calculations.

Know what works

See what actually works — and what doesn't.

How it works

From idea to insight in minutes, not weeks.

Describe your strategy

Enter your rules in plain English — entries, exits, risk, sessions.

Pick your market and timeframe

Choose the instruments and historical period to test against.

Run the backtest

One click. Results in seconds. No coding, no waiting.

Review and refine

Analyse performance, adjust rules, and re-test until you find your edge.

Built for traders, not programmers

You know your strategy. We handle the technical stuff.

Discretionary traders

Test your setups before risking real capital

Rule-based traders

Validate your system with hard data, not gut feel

Traders stuck in Excel

Finally move beyond spreadsheets and manual tracking

Join the Waitlist

Sign up to be the first to know when we launch.